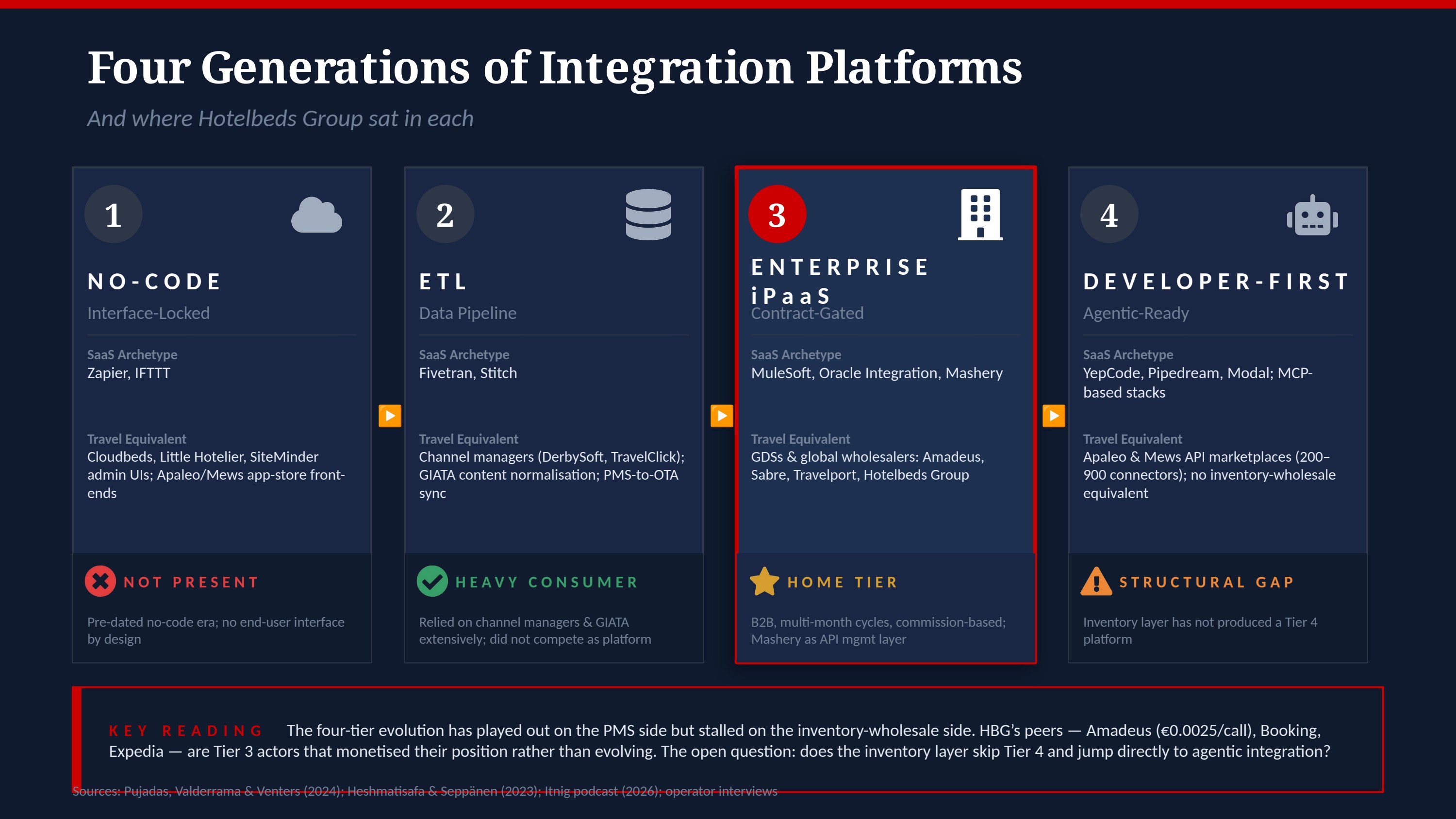

Across two decades of platform evolution, integration architecture has moved through four distinct generations. Each generation produced a dominant SaaS archetype, a travel-industry equivalent, and a clear position for Hotelbeds Group (HBG) to occupy — or to skip.

1 · No-code · Interface-locked

SaaS archetype: Zapier, IFTTT. Travel equivalent: Cloudbeds, Little Hotelier, SiteMinder admin UIs; Apaleo and Mews app-store front-ends.

HBG position — Not present. Pre-dated the no-code era; no end-user interface by design.

2 · ETL · Data pipeline

SaaS archetype: Fivetran, Stitch. Travel equivalent: Channel managers (DerbySoft, TravelClick); GIATA content normalisation; PMS-to-OTA sync.

HBG position — Heavy consumer. Relied on channel managers and GIATA extensively; did not compete as a platform.

3 · Enterprise iPaaS · Contract-gated

SaaS archetype: MuleSoft, Oracle Integration, Mashery. Travel equivalent: GDSs and global wholesalers — Amadeus, Sabre, Travelport, Hotelbeds Group.

HBG position — Home tier. B2B, multi-month cycles, commission-based; Mashery used as API-management layer.

4 · Developer-first · Agentic-ready

SaaS archetype: YepCode, Pipedream, Modal; MCP-based stacks. Travel equivalent: Apaleo and Mews API marketplaces (200–900 connectors); no inventory-wholesale equivalent.

HBG position — Structural gap. The inventory layer has not produced a Tier-4 platform.

Key reading

The four-tier evolution has played out on the PMS side but stalled on the inventory-wholesale side. HBG’s peers — Amadeus (€0.0025 per call), Booking, Expedia — are Tier-3 actors that monetised their position rather than evolving. The open question: does the inventory layer skip Tier 4 and jump directly to agentic integration?

Sources: Pujadas, Valderrama & Venters (2024); Heshmatisafa & Seppänen (2023); Itnig podcast (2026); operator interviews.